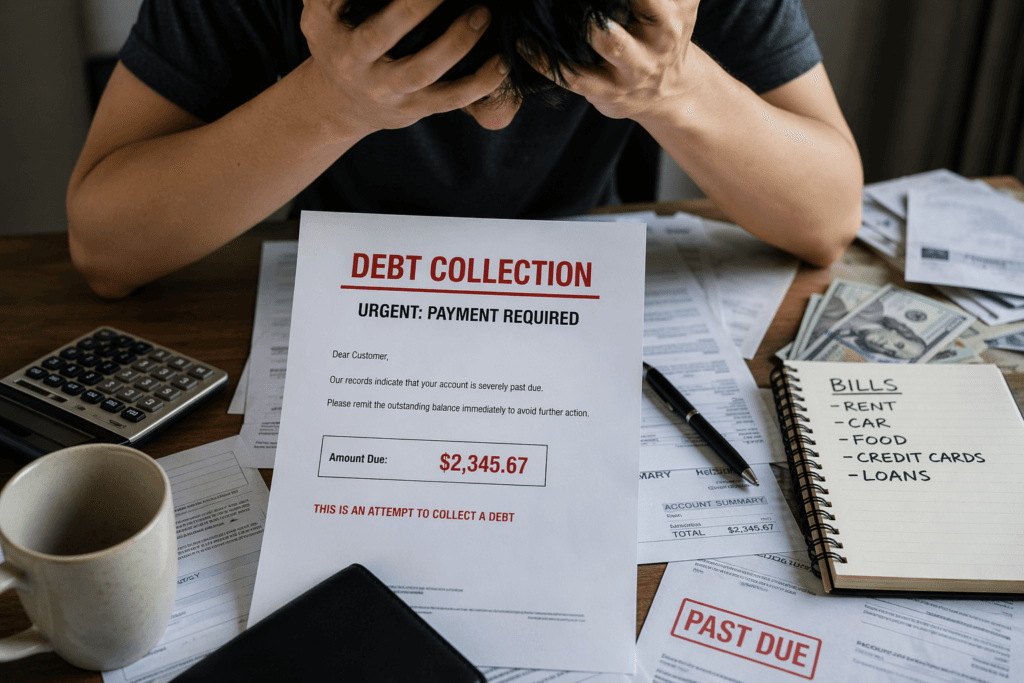

Getting a call from a debt collector is one of the most stressful financial experiences an American can face. The instinct for many people is simple: ignore it and hope it disappears.

It won’t.

Ignoring a debt collection agency doesn’t make the debt go away — it often makes the situation significantly worse. Before you decide to go silent on that collector, you need to understand the real consequences, your legal rights, and the smarter moves available to you.

Here’s a complete breakdown of exactly what happens when you don’t pay a collection agency in the United States.

How Does a Debt End Up in Collections in the First Place?

When you fall behind on payments — whether it’s a credit card, medical bill, personal loan, or utility account — your original creditor will typically wait 90 to 180 days before taking action. After that window, they usually do one of two things: they either sell the debt to a third-party collection agency for a fraction of what you owe, or they hire a collection company to recover the money on their behalf.

Once a collection agency owns or is working your debt, they are highly motivated to collect. Many agencies purchase debts for as little as pennies on the dollar, which means even a partial payment can be profitable for them — and that’s important to understand when it comes to negotiating later.

The 5 Real Consequences of Not Paying a Collection Agency

1. Your Credit Score Takes a Serious Hit

The moment a collection account is reported to the three major credit bureaus — Equifax, Experian, and TransUnion — your credit score drops. For someone with good credit, a single collection account can cause a drop of 100 points or more. For someone already working with fair credit, the damage can be just as devastating.

Under the Fair Credit Reporting Act (FCRA), a collection account can remain on your credit report for up to seven years from the date of your first missed payment that triggered the collection. That’s seven years of difficulty getting approved for a mortgage, car loan, apartment rental, or even some jobs.

One important nuance: even if you eventually pay the debt, the collection account doesn’t automatically disappear from your report. It will be updated to show “paid in full” or “settled,” which looks better to future lenders — but the record itself stays.

2. The Debt Keeps Growing

Many people assume that ignoring a debt freezes the amount owed. That’s not how it works.

Under the Fair Debt Collection Practices Act (FDCPA), a collection agency can continue charging the interest rate and any fees that were outlined in your original contract with the creditor. They cannot invent new fees or increase your rate — but if your original credit card agreement had a 24% APR, that interest may keep compounding while you ignore the collector’s calls.

This means the longer you wait, the more expensive the eventual resolution becomes.

3. Relentless Contact — Legally Allowed Up to a Point

Debt collectors are permitted to contact you by phone, mail, text, and email between 8 a.m. and 9 p.m. in your local time zone. They can also, in some circumstances, contact family members or neighbors — not to discuss your debt, but to locate you if they can’t reach you directly.

The FDCPA gives you the right to send a written “cease communication” letter, which legally requires the collector to stop contacting you. However, this is not the same as making the debt go away. They can still sue you. Sending a cease letter simply stops the phone calls and letters — it does not erase what you owe.

4. You Could Get Sued

This is the consequence most people don’t take seriously enough — and it’s the one with the most lasting damage.

If you ignore a collection agency long enough, they may decide to file a civil lawsuit against you. If they win — or if you simply don’t respond to the lawsuit — the court issues a default judgment in their favor. A default judgment is essentially the court saying: “The debtor didn’t show up to defend themselves, so the collector wins.”

Once a collector has a court judgment against you, they gain powerful legal tools:

- Wage garnishment — Up to 25% of your disposable income can be withheld directly from your paycheck and sent to the creditor, under federal law.

- Bank account levy — The collector can freeze and withdraw funds from your bank account.

- Property lien — A legal claim can be placed on your home or other assets, which must typically be resolved before you can sell the property.

Court judgments can remain enforceable for years and, in many states, can be renewed. This is not a situation you want to find yourself in.

5. It Affects More Than Just Your Credit

A collection account on your credit report doesn’t only affect your ability to borrow money. Landlords routinely check credit before approving rental applications. Employers in certain industries — finance, government, and security — may review credit as part of background checks. Even car insurance rates in some states are influenced by credit history.

The ripple effects of an ignored collection account can reach into corners of your life that have nothing to do with borrowing. Many top-tier financial tools — including the Best Rewards Credit Cards for 2026: Earn More Cash Back & Travel Points — are only available to people with strong credit profiles, which collection accounts can seriously damage.

Can You Actually Go to Jail for Not Paying?

No. Failing to pay a debt collection agency is not a criminal offense. You cannot be arrested simply because you owe money to a collector.

There are narrow exceptions: unpaid child support, significant tax debt owed to the IRS, and in rare cases, ignoring a direct court order (such as a subpoena for financial documents) can theoretically result in civil contempt. But for standard consumer debt — credit cards, medical bills, personal loans — non-payment is a civil matter, not a criminal one. Any collector who implies otherwise is violating the FDCPA.

What Is the Statute of Limitations on Debt?

Every state sets a statute of limitations on how long a creditor or collector has to sue you for an unpaid debt. This time frame varies by state and type of debt, typically ranging from three to six years, though some states allow up to ten years.

Once the statute of limitations expires, the debt becomes “time-barred” — meaning the collector can no longer win a lawsuit to collect it. However, there are two critical things to understand:

The debt still exists. Time-barred doesn’t mean forgiven. The collector can still contact you and ask for payment. They just can’t successfully sue you for it.

Making a payment can restart the clock. In many states, making even a single small payment on an old debt — or even verbally acknowledging that you owe it — can reset the statute of limitations, giving the collector a fresh window to sue you. Before making any payment on old debt, know your state’s laws or consult a credit counselor.

What Are Your Rights Under the FDCPA?

The Fair Debt Collection Practices Act is federal law that governs how third-party collectors can behave. Key protections include:

- Collectors cannot call before 8 a.m. or after 9 p.m.

- They cannot use abusive, threatening, or harassing language

- They cannot falsely claim to be attorneys or government officials

- They cannot threaten you with arrest for unpaid consumer debt

- They must send you a written validation notice within five days of first contact, telling you the amount owed, the name of the creditor, and your right to dispute the debt

If a collector violates the FDCPA, you have the right to sue them in federal court and may be entitled to damages up to $1,000 plus attorney fees.

What Should You Actually Do?

Ignoring the situation is almost never the best strategy. Here are the smarter moves available to you:

Request debt validation first. Before you pay anything or agree to anything, send a written request asking the collector to validate the debt. They must provide documentation proving you owe the amount they claim. This also protects you from paying debts you don’t actually owe or that have already been settled.

Negotiate a settlement. Collection agencies frequently purchase debts for 30 to 50 cents on the dollar. That means there is often significant room to negotiate. Many collectors will accept a lump-sum settlement for 40% to 60% of the original balance. Always get any agreement in writing before sending payment.

Ask about a pay-for-delete agreement. In some cases, collectors will agree in writing to remove the collection account from your credit report in exchange for payment. This isn’t guaranteed, and not all collectors will agree to it, but it’s worth asking — especially if the account is recent and significantly damaging your score.

Set up a payment plan. If you can’t settle in full, most agencies will work out a monthly payment arrangement. This stops the escalation and shows good faith if the situation ever reaches a courtroom.

Contact a nonprofit credit counselor. If your debt situation feels overwhelming, a nonprofit credit counseling agency — such as those affiliated with the National Foundation for Credit Counseling — can review your full financial picture and help you create a plan at no charge.

Consult a bankruptcy attorney if necessary. If you’re facing a lawsuit, wage garnishment, or multiple collections simultaneously, a bankruptcy attorney can explain whether Chapter 7 or Chapter 13 filing makes sense for your situation. Many offer free consultations.

The Bottom Line

Ignoring a debt collection agency is one of the most financially damaging things an American can do. The debt doesn’t disappear — it grows. The collector doesn’t give up — they escalate. And the consequences, from credit damage to wage garnishment, can follow you for years.

The smarter path is always to understand what you owe, know your rights under the FDCPA, and take deliberate action — whether that’s disputing the debt, negotiating a settlement, or setting up a payment plan you can actually afford.

Facing the situation head-on is uncomfortable. But it is almost always better than the alternative.

This article is for informational purposes only and does not constitute legal or financial advice. If you are facing a debt collection lawsuit or wage garnishment, consult a licensed attorney in your state.

Mohammad Javed is the founder and personal finance writer behind FinanceBeliever.com. He holds a Master of Commerce (MCom) degree with a specialization in finance and financial markets. Through years of personal experience studying credit systems, debt management, investment strategies, and how everyday financial decisions impact real households, he built Finance Believer to deliver straight, research-backed financial guidance to American readers. Every article he writes is sourced from authoritative data — including the Federal Reserve, the Consumer Financial Protection Bureau, and the Bureau of Labor Statistics. His work covers credit scores, loans, banking, insurance, investing, and personal budgeting — all written in plain English without the jargon.