Let’s be honest about something: you can do everything right as a driver — clean record, good credit, no accidents — and still pay more than twice what your cousin in another state pays for the exact same coverage. Not because you’re a riskier driver. Just because of your zip code.

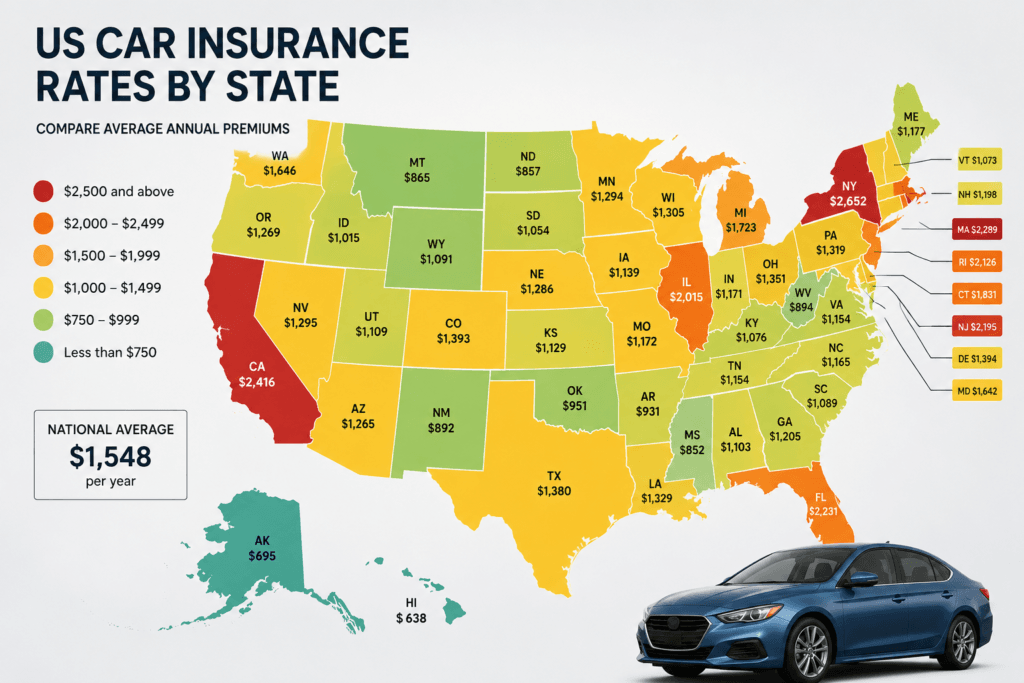

Car insurance rates in 2026 are more geographic than almost anything else in personal finance. According to Penny Pincher’s 2026 state-by-state rate analysis, average full coverage car insurance ranges from around $1,236 annually in Idaho and Vermont to over $4,300 in Florida and New York — a difference of over $3,000 per year for drivers with identical profiles.

That’s not a minor variation. That’s a car payment. Or a month and a half of groceries. Or a significant chunk of a vacation. Every single year.

This guide ranks the 10 cheapest states for car insurance in 2026, explains why some states are so much cheaper than others, breaks down the most expensive states you’ll want to avoid if cost matters, and gives you real strategies to lower your rate no matter where you currently live.

The National Average — Where Things Stand in 2026

Before the rankings, context matters.

According to Insurance.com’s April 2026 rate analysis, the national average cost of full coverage car insurance is $2,578 a year — or $215 a month — and all of the cheapest states have rates well below that figure. For minimum coverage only, the national average runs significantly lower, but most drivers with a financed or leased vehicle are required to carry full coverage anyway.

According to BeInsure’s May 2026 data, average premiums are expected to stabilize in 2026 compared to the brutal 17% surge in 2024, with only a 1% average increase anticipated nationally — and more than 50% of states are actually expected to see rates drop this year. That’s genuinely good news after two years of relentless premium increases.

Still, the gap between cheapest and most expensive states is enormous — and understanding where you fall on that map is the starting point for doing something about it.

The 10 Cheapest States for Car Insurance in 2026

#1 — Idaho: ~$1,236–$1,473/year

Idaho has claimed the top spot or near the top consistently for years. Low population density, minimal traffic congestion, fewer severe weather events than most states, and a relatively low rate of uninsured drivers all combine to keep claims frequency and cost lower than the national average.

According to BeInsure’s 2026 analysis, Idaho offers the lowest average car insurance rates in the US, with full coverage around $1,443 and minimum coverage at just $375 annually. For a driver in Florida paying $4,300+, moving to Idaho would save over $2,800 a year — more than $230 per month — for identical coverage.

#2 — Vermont: ~$1,236–$1,660/year

Vermont is the rare state where everyone seems to agree: cheap car insurance. The state has a small population, minimal urban congestion, low auto theft rates, and a culture that tends toward careful driving. According to Insurance.com’s 2026 data, Vermont is one of the cheapest states for car insurance at $1,660 for full coverage annually — well below the $2,578 national average.

Three companies in Vermont have average rates below $1,000 per year: Union Mutual, USAA, and Progressive — making Vermont one of the few states where even full coverage can cost less than $100 a month with the right insurer.

#3 — Maine: ~$1,367–$1,808/year

Maine rounds out the consistent top three cheapest states. Low population, minimal traffic, and a relatively small number of licensed drivers compared to other states keep claims down and rates low. According to US News Insurance’s 2026 analysis, Maine’s average annual premium of $1,367 makes it one of the cheapest states for car insurance, with several companies including USAA and Progressive offering rates below $1,000.

#4 — New Hampshire: ~$1,689/year

New Hampshire has the unusual distinction of being the only state in the continental US that doesn’t legally require drivers to carry auto insurance — though drivers who cause accidents are still financially responsible for damages. That regulatory environment, combined with low population density and minimal severe weather, keeps rates consistently below the national average. Full coverage averages around $1,689 per year according to Insurance.com’s 2026 data.

#5 — Wyoming: ~$1,356/year

Wyoming’s combination of low population, wide open roads, and minimal urban accident zones makes it one of the most affordable states for auto insurance. According to US News’ analysis, Wyoming has the third-lowest average annual premium at $1,356, with companies like American National offering rates as low as $682 per year in the state — extraordinarily cheap even by the standards of this list.

#6 — Ohio: ~$1,783–$1,842/year

Ohio is the surprise entry on this list — it’s a large, populous Midwestern state, which usually pushes rates higher. But Ohio’s mix of rural and suburban roads, relatively low severe weather claims, and strong insurer competition keeps premiums reasonable. According to Bankrate’s 2026 state-by-state analysis, Ohio drivers pay $1,842 per year for full coverage on average, significantly below the national average.

#7 — Hawaii: ~$1,361–$1,757/year

Hawaii surprises people. It’s expensive to live there, but car insurance is cheap — because the island geography limits how far cars travel, reduces highway speed accidents, and creates a naturally contained driving environment with fewer catastrophic multi-car pileups. According to multiple 2026 sources, Hawaii’s average full coverage rate runs around $1,757 per year.

#8 — Iowa: ~$1,800–$1,900/year

Iowa benefits from low population density, minimal traffic congestion, and roads designed for rural driving rather than urban commuting. BeInsure’s 2026 data highlights Iowa as one of the states expected to see the biggest rate decreases in 2026 — a 6.19% projected drop — which could push it even further down the cost rankings by year’s end.

#9 — North Dakota: ~$1,800–$1,950/year

North Dakota drivers pay roughly 33% less than the average American for full coverage car insurance. According to Bankrate’s analysis, North Dakota’s cheap rates are attributed to low instances of fatal crashes, low population density, and ninth-best highway infrastructure in the country according to the Reason Foundation study.

#10 — Wisconsin: ~$1,900–$2,000/year

Wisconsin rounds out the top 10 with rates that, while just under the national average, represent genuine savings compared to high-cost states. Rural landscape, relatively low auto theft rates, and strong insurer competition across the state keep Wisconsin consistently in the affordable tier.

Full Comparison: Cheapest vs. Most Expensive States in 2026

| State | Avg. Full Coverage/Year | vs. National Avg. |

|---|---|---|

| Idaho | ~$1,443 | -44% cheaper |

| Vermont | ~$1,506 | -42% cheaper |

| Maine | ~$1,651 | -36% cheaper |

| New Hampshire | ~$1,689 | -34% cheaper |

| Wyoming | ~$1,356 | -47% cheaper |

| Ohio | ~$1,842 | -29% cheaper |

| Hawaii | ~$1,757 | -32% cheaper |

| National Average | ~$2,136–$2,578 | — |

| Colorado | ~$3,100+ | +44% more expensive |

| Nevada | ~$4,000+ | +87% more expensive |

| Florida | ~$4,300+ | +100% more expensive |

| New York | ~$4,031+ | +88% more expensive |

| Louisiana | ~$4,300+ | +100% more expensive |

Why Are Some States So Much More Expensive?

The same coverage costs three times more in Florida than in Idaho. Here’s what actually drives that difference:

Population density and traffic. More cars on the road means more accidents. More accidents mean more claims. More claims mean higher premiums for everyone. Florida, New York, and California’s metro areas generate enormous claims volume.

Weather and natural disasters. Louisiana and Florida face hurricanes, flooding, and hail that total thousands of vehicles every year. Colorado’s hailstorms alone can cost insurers hundreds of millions per season. Those losses get priced into every policy in the state.

Uninsured driver rates. States with high rates of uninsured drivers push premiums up for everyone who does carry insurance. Florida consistently has one of the highest uninsured driver rates in the country — and every insured driver effectively subsidizes that risk.

No-fault vs. at-fault insurance systems. In no-fault states, your own insurance pays your medical bills after an accident regardless of who caused it. This increases the total claims paid by insurers and drives up rates. Florida is a no-fault state — which partially explains why it’s among the most expensive.

Legal environment and litigation costs. States with more aggressive personal injury litigation see insurers paying larger settlements more frequently. Those costs flow directly into premiums. Louisiana’s reputation as a litigation-friendly state is a major driver of its consistently high insurance costs.

Auto theft rates. States with higher vehicle theft rates — certain metro areas in California, Nevada, and Colorado — pay more because insurers expect a higher chance of total theft losses.

You Can’t Move States — But You Can Still Lower Your Rate

Most people reading this aren’t going to relocate to Idaho to save on car insurance. So here’s what actually works regardless of where you live:

Shop and compare every year. This is the single most impactful thing most people never do. According to ValuePenguin’s 2026 research, of the major national companies, American Family is the cheapest for full coverage — but you may find a better deal with a local or regional company, which is why getting quotes from multiple companies before buying is essential. Loyalty doesn’t pay in car insurance. Comparing does.

Raise your deductible. Increasing your deductible from $500 to $1,000 on comprehensive and collision coverage typically reduces your premium by 10% to 20%. This works best for drivers with a clean record and enough savings to cover the higher deductible if needed.

Bundle with renters or homeowners insurance. Most major insurers offer 5% to 15% discounts for customers who bundle auto with another policy. If you’re already paying for renters insurance — and you should be, as our complete guide on what renters insurance covers after a car break-in explains — ask your insurer about bundling both policies for a discount on each.

Ask about discounts you’re missing. Good student discount, low mileage discount, defensive driving course discount, paperless billing discount, autopay discount — many drivers qualify for several of these and never ask. A quick call to your insurer can surface savings you’re currently leaving on the table.

Maintain a clean driving record. A single at-fault accident can raise your premium 30% to 50% at renewal. Safe driving is the best long-term cost control strategy available — and in expensive states like Florida and New York, it’s even more valuable because the dollar impact of a rate increase is so much larger.

Check your credit score. In most states, insurers use your credit score as a rating factor. Improving your credit score can meaningfully reduce your car insurance premium. If you’re also paying high rates on a car loan, our guide on what qualifies as a good APR for a car loan in 2026 covers the overlap between credit and your total vehicle ownership cost.

The Bottom Line

Where you live matters — a lot — when it comes to car insurance. But short of relocating to Vermont or Idaho, the biggest lever you have is comparing rates aggressively, bundling policies, maintaining a clean record, and asking your insurer every year whether you’re getting the best rate available.

The national average is $2,136 to $2,578 per year. If you’re paying significantly more than that — and millions of Americans in Florida, New York, Louisiana, and Nevada are — you’re not stuck. You’re just not shopping yet.

FAQ

Q1: What is the cheapest state for car insurance in 2026? A1: Idaho and Vermont consistently rank as the cheapest states for full coverage car insurance in 2026, with average annual premiums around $1,236 to $1,506 — roughly 40% to 47% below the national average of $2,136 to $2,578. Wyoming, Maine, and New Hampshire are also consistently among the five cheapest states.

Q2: What is the most expensive state for car insurance in 2026? A2: Florida, Louisiana, and New York consistently rank as the most expensive states for car insurance in 2026, with average full coverage premiums ranging from $4,031 to $4,300+ annually. Nevada and Colorado also rank well above the national average, driven by high theft rates, severe weather, and litigation costs.

Q3: Why is car insurance so much cheaper in some states than others? A3: The primary drivers are population density, weather and natural disaster risk, uninsured driver rates, no-fault vs. at-fault insurance laws, and the legal environment for personal injury claims. States with low population density, minimal severe weather, and low litigation rates — like Idaho, Vermont, and Wyoming — consistently have the lowest premiums.

Q4: How can I lower my car insurance rate if I live in an expensive state? A4: The most effective strategies are comparing quotes from multiple insurers annually, bundling auto with renters or homeowners insurance, raising your deductible, maintaining a clean driving record, and improving your credit score. In high-cost states, these strategies can save hundreds of dollars per year even when the state average stays high.

Q5: Does moving to a cheaper state actually lower your car insurance? A5: Yes — significantly. A driver with the same profile, vehicle, and coverage moving from Florida to Idaho could save more than $2,800 per year. However, rates are based on where your vehicle is garaged, so you must update your policy with your new address when you move. Failing to update your address can result in a claim denial if an accident occurs.

DISCLAIMER

Car insurance rate data in this article is based on published 2026 averages from Insurance.com, BeInsure, US News, Bankrate, ValuePenguin, and Penny Pincher. Actual rates vary by driver profile, vehicle, coverage level, insurer, and ZIP code. Always get personalized quotes from multiple insurers for your specific situation.

Mohammad Javed is the founder and personal finance writer behind FinanceBeliever.com. He holds a Master of Commerce (MCom) degree with a specialization in finance and financial markets. Through years of personal experience studying credit systems, debt management, investment strategies, and how everyday financial decisions impact real households, he built Finance Believer to deliver straight, research-backed financial guidance to American readers. Every article he writes is sourced from authoritative data — including the Federal Reserve, the Consumer Financial Protection Bureau, and the Bureau of Labor Statistics. His work covers credit scores, loans, banking, insurance, investing, and personal budgeting — all written in plain English without the jargon.