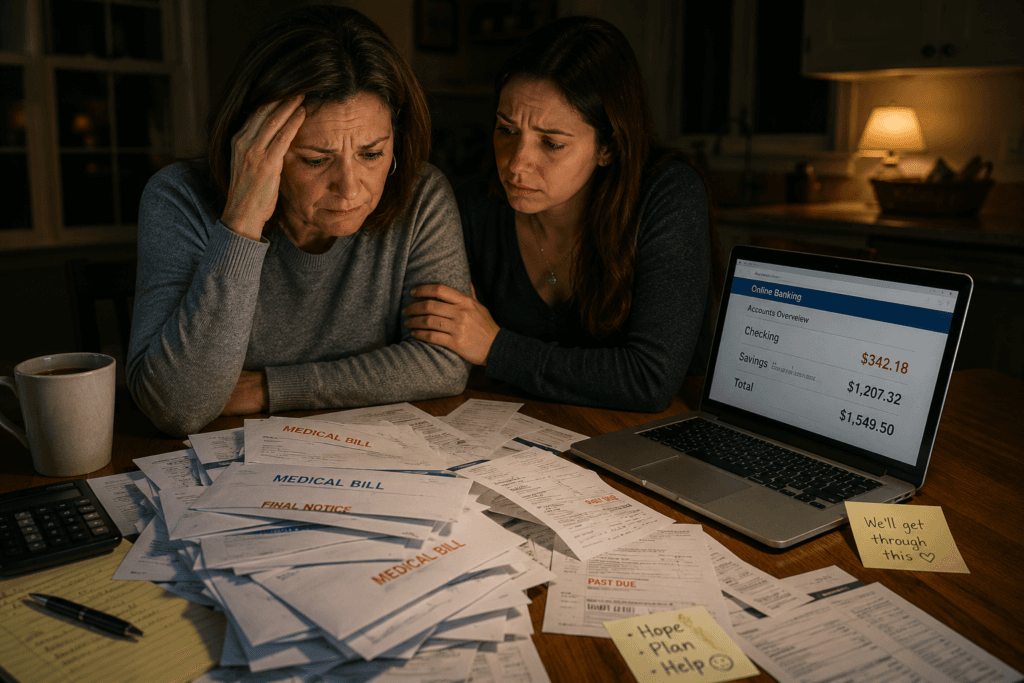

The bill arrives. Maybe it’s $800. Maybe it’s $8,000. Maybe it’s more. You look at your bank account, and then you look at the bill, and the math just doesn’t work. So you set it on the counter, tell yourself you’ll figure it out later, and try not to think about it.

Most Americans in this situation do exactly the same thing. And most of them don’t actually know what happens next — whether ignoring it will catch up to them, how bad the damage really gets, or what options they actually have.

Here’s the honest answer, step by step.

First, You’re Not Alone — Not Even Close

Nearly one in three Americans currently carries medical debt. According to a 2026 analysis, an estimated 4.8 million Americans lost medical coverage in January 2026 alone when ACA subsidies expired and insurance companies raised rates by an estimated 26%. That’s millions of people suddenly facing medical costs without the coverage they had before.

So whatever you’re feeling about that bill sitting on your counter right now — shame, panic, the urge to pretend it doesn’t exist — understand that this is a national crisis, not a personal failure.

The Real Timeline: What Actually Happens

Days 1–60: The Grace Period Nobody Tells You About

When you first receive a medical bill, nothing catastrophic happens immediately. Providers send statements and reminders. During this window, according to the Consumer Financial Protection Bureau, this is also the most important time to act — because you have the most leverage and the most options right now.

Use this window to do two things: verify the bill is actually correct (medical billing errors are shockingly common — one 2026 source puts the error rate above 70%), and contact the billing department to discuss your situation. Most providers would rather work with you than send your account to collections.

Days 60–120: Final Notices and Escalating Pressure

If the bill stays unpaid, you’ll start receiving final notice letters and more frequent calls from the provider’s billing department. Fidelity’s financial guidance notes that after 60 to 120 days past due, providers will typically move to the next step — collections.

This is still not the end of the world. You can still negotiate. You can still set up a payment plan. You can still apply for financial assistance. But the window is narrowing.

After 120 Days: Collections

Once a medical bill hits roughly 120 days unpaid, most providers sell or transfer the debt to a third-party collection agency. At this point, the dynamic changes significantly.

Debt collectors will contact you by phone, mail, and email. They’re persistent by design. However — and this is important — they are legally required to follow the Fair Debt Collection Practices Act (FDCPA). They cannot harass you, threaten you, call at unreasonable hours, or misrepresent what you owe. You also have the right to request written verification of the debt, and if there are errors, you can dispute them. Don’t let a debt collector bully you into paying something you don’t actually owe or something that’s been inflated with fees.

The Credit Score Damage — And the Recent Rule Change

Here’s where a lot of people expect the worst, and the reality in 2026 is actually somewhat better than it used to be.

As of 2023, medical debts under $500 do not appear on your credit report at all. Medical debts less than one year old also don’t appear. According to CBS News’ analysis, providers can technically sue for any amount, but for smaller balances it’s rarely worth the cost of legal action.

For larger debts — over $500 and over a year old — the damage can be significant. A medical collection on your credit report can stay there for up to seven years and cause a meaningful drop in your credit score. If you’re working on rebuilding credit or planning to apply for a mortgage, this matters a lot. Check out our guide on what credit score you need to buy a house in 2026 to understand the stakes clearly.

Lawsuits and Wage Garnishment — The Worst Case

Yes, providers and collection agencies can sue you for unpaid medical debt. If they win, courts can authorize wage garnishment — automatic deductions from your paycheck — or in some states, place liens on property.

The reality: lawsuits are significantly more likely for large balances where other collection attempts have failed. According to research cited by the PMC (National Library of Medicine), approximately 25% of high-income hospitals in the US are known to sue patients for unpaid bills. That’s not a small number. Ignoring a bill entirely — especially a large one — is genuinely risky.

One thing that will not happen: you cannot be arrested or jailed for unpaid medical bills. Medical debt is a civil matter, not a criminal one. If a debt collector ever threatens you with arrest, that’s a violation of the FDCPA — document it and report it.

What You Can Actually Do About It

Step 1: Check the Bill Before You Pay Anything

Medical billing errors are more common than most people realize. Ask for an itemized bill — a line-by-line breakdown of every charge. Look for duplicate charges, incorrect billing codes, services marked as out-of-network that weren’t, and procedures you don’t recognize. If you have insurance, make sure the bill reflects what the insurer paid, not just the gross amount.

The No Surprises Act, still in effect in 2026, protects you from unexpected out-of-network charges for emergency services. If you see out-of-network charges for care you reasonably believed was in-network, dispute them immediately with both the provider and your insurer.

Step 2: Call the Billing Department and Negotiate

This is the step most people skip because it feels uncomfortable. It’s also the most powerful thing you can do.

Medical billing departments have more flexibility than people realize. You can negotiate a reduced balance — especially if the account has aged or is heading toward collections, when getting something is better than getting nothing. According to Coventry Direct’s 2026 debt guide, a simple phone call asking whether the balance can be reduced can lead to real savings.

Ask specifically about:

- Prompt pay discounts — paying in full immediately, even a lower negotiated amount

- Charity care or financial assistance — nonprofit hospitals are legally required to offer this under the ACA

- Income-based sliding scale discounts — many hospitals tier assistance based on your household income vs. the federal poverty level

Step 3: Set Up a Payment Plan

If you can’t pay in full, ask for a payment plan. Many providers offer interest-free payment plans — you just have to ask. You don’t necessarily need to prove financial hardship. Breaking a $3,000 bill into $100/month payments changes it from a crisis into something manageable.

If your debt has already gone to collections, you can still negotiate a payment plan directly with the collection agency, or sometimes negotiate a lump-sum settlement for less than the full amount owed.

Step 4: Apply for Hospital Financial Assistance

Every nonprofit hospital in the United States is required by the Affordable Care Act to have a financial assistance program — sometimes called “charity care.” Many people qualify and never apply because they don’t know it exists.

Eligibility is typically based on your household income relative to the federal poverty level. Some hospitals provide free care to patients at or below 200% of the poverty line. Others offer tiered discounts up to higher income levels. This isn’t charity in a humiliating sense — it’s a legal program these hospitals are required to maintain as a condition of their nonprofit status.

Call the billing department, ask specifically about financial assistance programs, and ask what documentation they need. The worst they can say is no.

Step 5: Check Government Programs

USA.gov lists both federal and state resources for medical bill assistance. Depending on your income and situation, you may qualify for Medicaid (which can sometimes cover retroactive medical costs), state-specific programs, or disease-specific nonprofit funds that cover treatment costs for particular conditions.

If your situation is dire, medical bankruptcy — specifically Chapter 7 — is a real option that discharges medical debt. It’s not without consequences, but for people crushed by six-figure medical debt, it’s a legal protection that exists for exactly this reason.

What NOT to Do

Don’t put medical debt on a credit card. Credit card interest rates are often 20%+ in 2026. You’re trading negotiable medical debt for high-interest consumer debt. Unless you have a 0% promotional offer and a clear payoff plan, this almost never helps.

Don’t tap your 401(k). Early withdrawals trigger a 10% penalty plus ordinary income tax. For most people, the math doesn’t work.

Don’t ignore it. This is the worst option of all. Ignoring limits your options, eliminates your negotiating leverage, accelerates the timeline to collections and lawsuits, and adds interest and fees. If you’re overwhelmed with debt in general, our guide on the best debt consolidation loans in 2026 may also be worth reading for your broader picture.

One More Thing Worth Knowing

Medical debt behaves differently from other types of debt. Unlike a car loan or credit card balance, it’s almost always negotiable. Providers set prices knowing they’ll rarely get the full billed amount — they negotiate with insurance companies constantly. A patient calling and saying “I genuinely cannot pay this, what can we work out?” is not an unusual situation for a billing department. You have more leverage than you think.

If you’ve already had medical debt hit your credit report, check out our guide on how to remove collections from your credit report — there are specific legal strategies for medical debt collections that are worth understanding.

Frequently Asked Questions

Can you go to jail for not paying medical bills in 2026? No. Medical debt is a civil matter, not a criminal one. You cannot be arrested or imprisoned for not paying a medical bill. If a debt collector ever threatens you with jail time, that is a violation of the Fair Debt Collection Practices Act — document it and report it to the CFPB.

How long before a medical bill goes to collections? Typically 90 to 120 days, though this varies by provider. Some providers wait up to 180 days before sending accounts to a collection agency. This is your window to negotiate directly with the billing department before collections get involved.

Does unpaid medical debt hurt your credit score in 2026? Medical debts under $500 no longer appear on credit reports at all as of recent rule changes. Debts less than one year old also don’t appear. However, larger debts over $500 that are more than a year old can appear on your credit report and stay there for up to seven years.

Can a hospital take your house for unpaid medical bills? In some states, if a court judgment is obtained after a successful lawsuit, a lien can be placed on property. This is a worst-case scenario that typically only occurs after other collection efforts have failed on large balances. It is rare but legally possible in certain states.

What is the best first step if you get a medical bill you can’t pay? Open it, request an itemized statement, verify every charge is accurate, and then call the billing department before anything else. Ask about financial assistance programs, payment plans, and any available discounts. Acting early gives you the most options and the most leverage.

This article is for informational purposes only and does not constitute financial, legal, or medical advice. If you are facing significant medical debt, consider consulting with a nonprofit credit counselor or attorney.

Mohammad Javed is the founder and personal finance writer behind FinanceBeliever.com. He holds a Master of Commerce (MCom) degree with a specialization in finance and financial markets. Through years of personal experience studying credit systems, debt management, investment strategies, and how everyday financial decisions impact real households, he built Finance Believer to deliver straight, research-backed financial guidance to American readers. Every article he writes is sourced from authoritative data — including the Federal Reserve, the Consumer Financial Protection Bureau, and the Bureau of Labor Statistics. His work covers credit scores, loans, banking, insurance, investing, and personal budgeting — all written in plain English without the jargon.