Here’s a scenario that plays out for millions of Americans every year.

You missed a payment — maybe during a job loss, a medical crisis, a divorce, or just a rough stretch of months. The debt went to collections. You eventually got back on your feet, maybe even paid it off. But the collection account is still sitting on your credit report like a scarlet letter, dragging your score down by 50 to 150 points, making every loan application harder, every interest rate higher, every financial step forward a little more expensive.

And someone told you: just wait seven years. It’ll fall off eventually.

That’s technically true. But it’s also terrible advice — because according to Rrova’s March 2026 credit repair guide, a single collection account can drop your credit score anywhere from 50 to 150 points depending on where your score starts — meaning if you had a 720 score, one collection could push you below 600, the threshold where most lenders start declining applications or charging significantly higher rates. Waiting seven years to fix that costs you real money every single year in the form of higher rates, declined applications, and missed financial opportunities.

You don’t have to wait. Here are the 4 legal methods to get collections removed from your credit report in 2026 — starting with the ones that work fastest.

What You’re Dealing With — The Basics

Before the methods, let’s make sure we’re talking about the same thing.

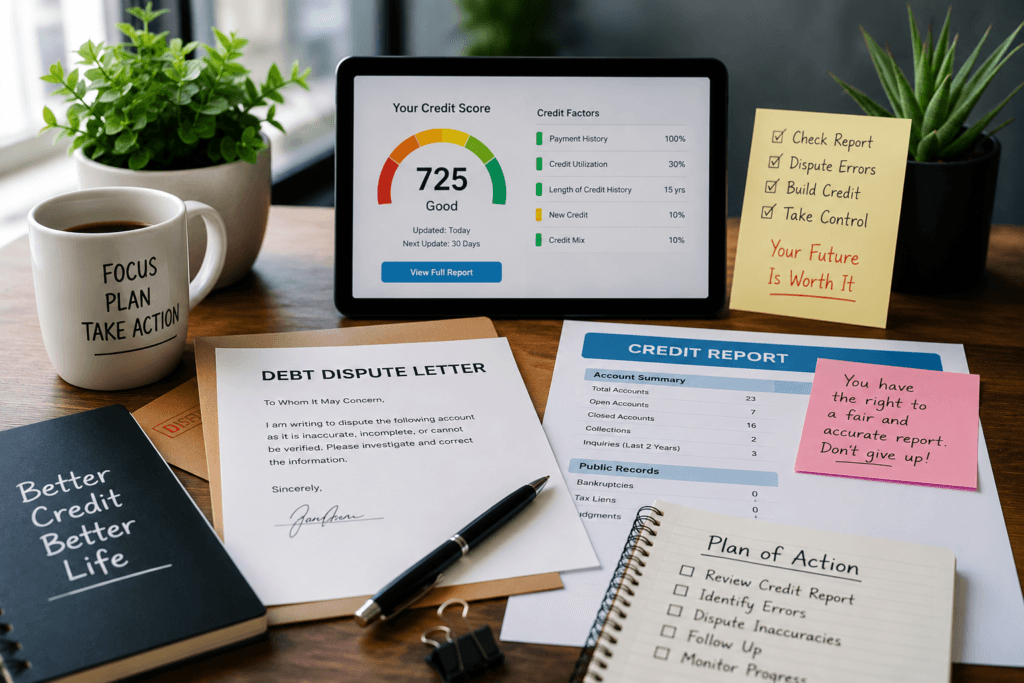

A collection account appears on your credit report when a creditor — a credit card company, medical provider, utility company, phone carrier — gives up trying to collect a debt you owe and sells or transfers it to a collection agency. That collection agency then has the right to pursue you for the debt and report the delinquency to the three major credit bureaus: Equifax, Experian, and TransUnion.

According to CreditWiseLife’s March 2026 collection guide, a collection account can remain on your credit report for up to 7 years from the original delinquency date — not from when the account was sold to the collector, not from when you were contacted, but from the date you first missed the payment that started the whole chain. This distinction matters because some collectors illegally try to “re-age” debts by reporting a more recent date — which is a Fair Credit Reporting Act violation you can use against them.

Now — here are your four options, ranked by how often they work.

Method 1 — Dispute Errors Under the FCRA (Highest Success Rate for Inaccurate Accounts)

The Fair Credit Reporting Act gives you the legal right to dispute any information on your credit report that is inaccurate, incomplete, or unverifiable. If a collection account contains any error — wrong balance, wrong date, wrong original creditor, duplicate entry, account that isn’t even yours — you can dispute it and the bureau is legally required to investigate and remove it if it can’t be verified.

Here’s the thing most people miss: according to Statush’s March 2026 FCRA guide, collection accounts frequently contain errors that make them legally disputable — incorrect balances, wrong delinquency dates, double reporting where both the original creditor and the collection agency are reporting an active balance for the same debt, and in many cases accounts that were sold multiple times and contain contradictory information across all three bureaus.

Pull your free credit reports from all three bureaus at AnnualCreditReport.com. For each collection account, look for:

- Wrong balance — if you paid $50 toward the debt and the report still shows the full original amount

- Wrong date of first delinquency — this is the clock that determines when the account falls off; an incorrect date is disputable

- Duplicate reporting — original creditor AND collection agency both showing active balances for the same debt

- Account not yours — identity errors are more common than people realize

- Debt beyond the 7-year window — if the date of first delinquency was over 7 years ago, the account must be removed immediately

How to file a dispute:

All three bureaus allow online disputes, phone disputes, or mail disputes. For anything involving documentation, certified mail with return receipt is safest — it creates a paper trail.

According to Discover’s collection removal guide, all three credit bureaus allow you to dispute errors online, by mail, or phone — and the bureau must investigate and respond within 30 days, either correcting, deleting, or verifying the account.

The dispute letter script:

“I am writing to dispute the following information on my credit report. The collection account listed from [Collection Agency Name], account number [XXXX], contains the following inaccurate information: [describe the specific error]. Under the Fair Credit Reporting Act, I request that this item be investigated and removed if it cannot be verified as fully accurate. I have enclosed [any supporting documentation].”

Send to each bureau where the error appears. Keep copies of everything.

Method 2 — Debt Validation Letter (Best First Step Before Paying Anything)

Before you pay a single dollar on any collection account — and before you dispute with the bureaus — send the collection agency a debt validation letter.

Under the Fair Debt Collection Practices Act (FDCPA), you have the right to request that a collection agency prove the debt is valid and that they have the legal authority to collect it. According to CreditWiseLife’s 2026 guide, you have the right to request debt validation from the collection agency, including proof of the debt, original creditor details, and the exact amount owed — and if the collector cannot verify the debt, they must remove it from your credit report and stop collection efforts.

This works particularly well on:

- Old debts that have changed hands multiple times

- Medical debts where billing errors are extremely common

- Debts where the collection agency bought a large portfolio and may have incomplete records

The debt validation letter script:

“I am writing in response to your collection notice regarding account [number]. I am requesting that you provide validation of this debt, including: (1) the name and address of the original creditor, (2) a copy of the original signed agreement or documentation showing I owe this debt, (3) proof that your agency is licensed to collect debt in my state, and (4) the exact amount claimed to be owed with an explanation of all fees and interest added. Until this debt is validated, please cease all collection activity including credit bureau reporting.”

Send via certified mail. If the collection agency cannot validate the debt, they are legally required to stop reporting it — which means you can then dispute it with the credit bureaus as unverifiable, and it must be removed.

Method 3 — Pay-for-Delete Agreement (Best Option for Valid Debts You Can Afford to Pay)

If the debt is legitimately yours and valid, a pay-for-delete agreement is your most powerful negotiating tool.

A pay-for-delete is exactly what it sounds like: you offer to pay the collection account — often at a reduced settlement amount — in exchange for the collection agency agreeing in writing to delete the account from your credit report entirely. Not mark it as paid. Delete it.

According to DisputeAI’s January 2026 collections guide, a pay-for-delete agreement is when you negotiate with the collection agency to remove the account from your credit report in exchange for payment — and the strategy is to contact the agency in writing, offer to pay a portion (starting at 25% to 50% of the balance), and get the agreement in writing before paying a single dollar.

This last point cannot be overstated. Get the pay-for-delete agreement in writing before paying. Collection agencies have been known to accept payment and then not follow through on deletion. A written agreement gives you legal recourse if they don’t honor it.

The pay-for-delete script:

“I am willing to resolve this account by paying [offer amount — start at 25–40% of balance] as settlement in full, provided that [Collection Agency Name] agrees in writing to permanently delete this account from all three major credit bureau reports (Equifax, Experian, and TransUnion) within 30 days of payment receipt. Please respond in writing with your acceptance of these terms. I will not submit payment until a written agreement is received.”

Important reality check: not every collection agency will agree to pay-for-delete. Some have internal policies against it. But many will — especially for older debts and especially when you’re offering immediate settlement. According to DisputeAI, it never hurts to ask — many will negotiate, especially for older debts, and the worst answer you can get is no, which leaves you exactly where you started.

Also worth knowing: paying a collection without a delete agreement does not significantly help your score on older FICO models. On FICO 8 — still widely used by lenders — a “paid collection” is nearly as damaging as an “unpaid collection.” Pay-for-delete is superior to simply paying.

Method 4 — Goodwill Letter (Best for Paid Collections With a Legitimate Hardship Story)

If you’ve already paid the collection and it’s still showing on your report, a goodwill letter is your best remaining option.

A goodwill letter is a direct appeal to the collection agency or original creditor asking them to remove the negative mark as a courtesy — acknowledging that you’ve paid, explaining the circumstances that led to the original delinquency, and requesting that they extend goodwill by removing the account.

According to DisputeAI’s 2026 guide, goodwill letters work best when you have a good reason for the original delinquency — job loss, medical emergency, family crisis — you take responsibility in the letter, explain your circumstances politely, and ask for removal as a courtesy. This is not a legal right. The creditor is not obligated to remove a legitimate paid collection. But many do — especially original creditors who want to maintain customer goodwill, and especially when you frame the request respectfully.

The goodwill letter script:

“Dear [Creditor/Collection Agency], I am writing regarding the account [number] which appears on my credit report. I want to acknowledge that this account went delinquent due to [job loss/medical emergency/family hardship] — a situation I have since resolved. I have paid this account in full and have maintained a strong payment history on all my other accounts since that time. I am writing to respectfully request that you consider removing this account from my credit report as a gesture of goodwill. I recognize this is not required, but it would make a meaningful difference in my financial recovery. Thank you for your consideration.”

Send to both the collection agency and the original creditor if the account has been transferred. Follow up in 30 days if you don’t hear back. Some goodwill letters succeed on the second or third attempt.

The 2026 Medical Debt Rule — Important Update

If your collection is from a medical bill, there’s genuinely good news in 2026.

The three major credit bureaus — Equifax, Experian, and TransUnion — now exclude all medical debt under $500 from credit reports entirely. Paid medical collections are also excluded. This change was phased in through 2023 and 2024, and in 2026 it is fully in effect across all three bureaus.

If you have a medical collection under $500 on your report right now, file a dispute immediately — it should no longer be there, and the bureau is required to remove it.

For medical collections over $500, the same four methods above apply — but start with the goodwill letter approach, since medical debt hardship arguments tend to be more sympathetically received than other types of collections.

What Happens to Your Score After Removal

Here’s what to realistically expect once a collection is removed:

According to Rrova’s analysis, most clients see their first deletions within 30 to 45 days of starting the dispute process and hit their target score range within 90 days — though results depend heavily on what else is in your credit file.

The score recovery from removing a collection depends on:

- How recent the collection was (recent collections hurt more, so their removal helps more)

- How many other negative items remain on your report

- Your overall credit mix and history length

- Whether the collection was paid or unpaid before removal

A single recent collection removal can add 50 to 100+ points for someone with an otherwise clean file. For someone with multiple negative items, the improvement per removal is smaller but still meaningful — and cumulative as you work through each one.

Building From Here

Getting collections removed is one part of a bigger credit rebuild. Once the negative items are gone, the path forward is consistent positive history — on-time payments every month, low credit utilization, and ideally a mix of account types reporting actively.

And if some of the collections on your report stem from debt that went unpaid because the original situation was overwhelming, understanding your full rights in the collection process matters. Our breakdown of what actually happens when you don’t pay a debt collection agency covers the legal process from the collector’s side — which gives you much better context for the negotiation strategies above.

Your credit is not a fixed number. It’s a score that responds to specific actions — and the actions in this guide are exactly what move it.

Quick Reference: Which Method to Use

| Your Situation | Best Method |

|---|---|

| Collection contains any error at all | Method 1 — FCRA Dispute |

| Collection is old or from a company with poor records | Method 2 — Debt Validation Letter |

| Debt is valid and you can afford to settle | Method 3 — Pay-for-Delete |

| Already paid the collection | Method 4 — Goodwill Letter |

| Medical collection under $500 | Dispute immediately — should already be removed |

| Collection is over 7 years old | Dispute immediately — must be removed by law |

FAQ

Q1: Can you actually remove collections from your credit report before 7 years? A1: Yes — legally and often successfully. The four main methods are disputing inaccurate information under the FCRA, sending a debt validation letter to challenge unverifiable debts, negotiating a pay-for-delete agreement before paying, and sending a goodwill letter for already-paid collections. Collections that contain any error — wrong balance, wrong date, duplicate reporting — can be legally disputed and removed regardless of age.

Q2: What is a pay-for-delete agreement and does it work in 2026? A2: A pay-for-delete is an agreement where you offer to pay a collection account — often at a reduced settlement of 25% to 50% of the balance — in exchange for the collection agency deleting the account from your credit report entirely. It works for many collection agencies, especially on older debts. The critical rule: always get the agreement in writing before making any payment. Not all collection agencies will agree to pay-for-delete, but many will negotiate.

Q3: Does paying a collection improve your credit score? A3: On older scoring models like FICO 8, paying a collection without securing a delete agreement has minimal impact — a “paid collection” is nearly as damaging as an “unpaid collection.” On newer models like FICO 9 and FICO 10, paid collections are ignored entirely, which helps more. For maximum score improvement, pursue pay-for-delete rather than simply paying.

Q4: How long does it take to remove a collection from your credit report? A4: The credit bureaus have 30 days to investigate a dispute and respond. If the dispute is successful or the collection agency agrees to delete, the account typically disappears from your report within 30 to 45 days. Goodwill letters may take longer — 30 to 90 days — depending on how quickly the creditor responds.

Q5: What is a debt validation letter and when should I send one? A5: A debt validation letter is a written request to a collection agency demanding proof that the debt is valid, that they have the right to collect it, and that the amount is accurate. Under the Fair Debt Collection Practices Act, the collector must stop reporting the debt if they cannot validate it. Send a debt validation letter before paying any collection — especially for older debts, medical debts, or debts that have changed hands multiple times where documentation may be incomplete.

DISCLAIMER

This article is for educational purposes only and does not constitute legal or financial advice. Credit laws, bureau policies, and collection agency practices vary. For complex credit situations involving multiple collections, charge-offs, or potential FDCPA violations, consider consulting a nonprofit credit counselor or consumer law attorney.

Mohammad Javed is the founder and personal finance writer behind FinanceBeliever.com. He holds a Master of Commerce (MCom) degree with a specialization in finance and financial markets. Through years of personal experience studying credit systems, debt management, investment strategies, and how everyday financial decisions impact real households, he built Finance Believer to deliver straight, research-backed financial guidance to American readers. Every article he writes is sourced from authoritative data — including the Federal Reserve, the Consumer Financial Protection Bureau, and the Bureau of Labor Statistics. His work covers credit scores, loans, banking, insurance, investing, and personal budgeting — all written in plain English without the jargon.