Most budgeting advice fails beginners in the same way: it’s either so complicated it takes hours to set up, or so vague it doesn’t tell you what to actually do with your money.

The 50/30/20 rule solves both problems. It’s simple enough to calculate in five minutes, flexible enough to work on almost any income, and specific enough to actually change what you do with your paycheck.

According to The Penny Hoarder’s 2026 State of Savings survey, about 58% of Americans live paycheck to paycheck — and for most of them, the core issue isn’t how much they earn but the complete absence of a spending plan. A budget doesn’t fix your income. But it does tell every dollar where to go before you have a chance to spend it on something that doesn’t matter.

Here’s the complete guide to the 50/30/20 rule — what it is, how to calculate your numbers, what to do when the percentages don’t fit your life, and how to make it stick beyond the first month.

What Is the 50/30/20 Rule?

The 50/30/20 rule divides your after-tax income into three categories:

- 50% — Needs: Everything required to keep your household running — rent or mortgage, utilities, groceries, transportation, insurance, and minimum debt payments

- 30% — Wants: Everything that improves your life but isn’t essential — dining out, streaming services, hobbies, clothing beyond basics, travel, entertainment

- 20% — Savings and debt payoff: Emergency fund contributions, retirement savings, extra debt payments above minimums, and investment contributions

According to Citizens Bank’s budgeting guide, the 50/30/20 method is one of the most popular percentage-based budgeting frameworks because it gives your budget structure while still leaving room for flexibility — it’s not about strict limits, it’s about building balance.

The rule was popularized by US Senator Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan, and has become the go-to starting framework for Americans learning to budget for the first time.

Step 1 — Calculate Your After-Tax Monthly Income

The first step is figuring out your actual take-home pay — not your salary, but what actually hits your bank account each month after taxes and other withholdings.

If you’re a salaried employee: Check your most recent pay stub. Your net pay — the amount deposited — is your starting number. Multiply by how many paychecks you receive per month (2 if paid biweekly, 2.167 if you want to account for the occasional three-paycheck month).

If you’re hourly: Multiply your hourly rate by your average hours worked, then subtract the taxes withheld from your most recent check to calculate the actual percentage being taken out.

If you’re self-employed or freelance: Use your average monthly net income from the past three months. Because your income varies, take a conservative estimate — build your budget around your lower-income months, not your best ones.

One important note: According to Wealthvieu’s 2026 budgeting guide, one of the most common mistakes beginners make is using gross income instead of after-tax income — using your $75,000 salary instead of your $58,000 take-home inflates every budget category by 29% and sets you up to overspend from day one. Always start with the money that actually hits your account.

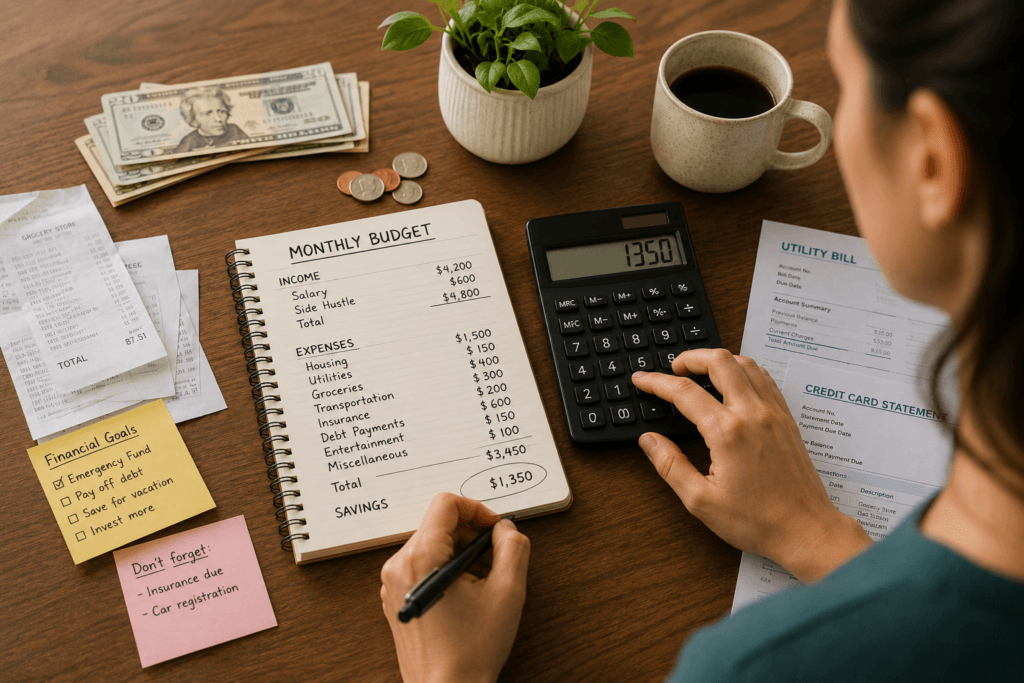

Example used throughout this guide: Monthly after-tax income: $4,500

Step 2 — Calculate Your Three Buckets

Once you have your monthly take-home, the math is straightforward:

| Category | Percentage | Monthly Amount (on $4,500) |

|---|---|---|

| Needs | 50% | $2,250 |

| Wants | 30% | $1,350 |

| Savings/Debt | 20% | $900 |

For the $4,500 example: $2,250 goes to needs, $1,350 to wants, and $900 toward savings and debt payoff every single month.

That’s the entire framework. The challenge isn’t the math — it’s categorizing your expenses honestly and then actually staying within the limits.

Step 3 — Categorize Every Monthly Expense

This is where most beginners get stuck, because the line between needs and wants is blurry. Here’s a clear breakdown:

What Counts as a NEED (50%)

| Category | Examples |

|---|---|

| Housing | Rent, mortgage payment, renter’s insurance, property tax |

| Utilities | Electricity, gas, water, internet (basic plan) |

| Food | Groceries (not restaurants) |

| Transportation | Car payment, gas, car insurance, bus/subway pass |

| Healthcare | Health insurance premiums, prescriptions, essential medical |

| Minimum debt payments | Credit card minimums, student loan minimums, personal loan minimums |

| Childcare | Daycare, school fees for children |

The key test for a need: Could you reasonably lose your job, housing, health, or ability to work without this expense? If yes, it’s a need.

What Counts as a WANT (30%)

| Category | Examples |

|---|---|

| Dining out | Restaurants, coffee shops, food delivery apps |

| Entertainment | Streaming services, concerts, sports events, movies |

| Shopping | Clothing beyond basics, home décor, gadgets |

| Travel | Vacations, weekend trips, flights |

| Subscriptions | Multiple streaming apps, gaming services, magazines |

| Gym memberships | When a free alternative exists |

| Upgrades | A $3,500 apartment when a $1,800 one would suffice |

That last example matters — according to Wealthvieu’s analysis, the average American spends 34% of income on housing alone in 2026, above the old assumption that all needs fit comfortably in 50%. If your rent already consumes 40% of take-home, every other “need” is competing for 10% — which forces honest choices about what’s truly necessary versus chosen.

What Counts as SAVINGS/DEBT (20%)

| Category | Examples |

|---|---|

| Emergency fund | Monthly contribution to your cash cushion |

| Retirement savings | 401(k) above the employer match, Roth IRA contributions |

| Extra debt payments | Any amount above the minimums on credit cards or loans |

| Investment contributions | Brokerage account, index funds |

| Sinking funds | Saving monthly for predictable future expenses (car repairs, holidays) |

The 20% bucket is the most important number in your entire budget. It’s what separates people who build financial security from people who stay stuck. According to NerdWallet’s 2026 Consumer Outlook Report, 46% of Americans plan on saving money for emergencies in 2026, and 30% plan on paying off at least one debt in full — but good intentions without a budget allocation almost never materialize into actual savings.

Step 4 — Compare Your Current Spending to the Targets

Now pull out your last month of bank and credit card statements and categorize every transaction.

Most people are surprised — sometimes shocked — by what they find. Common discoveries:

- Food delivery apps quietly consuming $200–$400 per month

- Subscriptions totaling $80–$180 that haven’t been reviewed in a year

- “Needs” like a premium apartment eating 40%+ of take-home

- The savings bucket sitting at 0%–3% instead of 20%

This audit is the most uncomfortable part of building a first budget. It’s also the most valuable. You can’t fix spending patterns you haven’t measured.

According to Fortune’s reporting on the 50/30/20 rule, financial planners at firms like Ritholtz Wealth Management use the 50/30/20 analysis as the starting point for every new client’s budget — not because the percentages are sacred, but because the framework forces you to see, often for the first time, exactly where your money is actually going.

Step 5 — Adjust and Make It Work For Your Real Life

Here’s the honest truth: the 50/30/20 rule is a target, not a law. For many Americans in 2026, hitting exactly 50/30/20 isn’t realistic right out of the gate — especially in high cost-of-living cities where rent alone exceeds 35% of take-home.

Here’s how to adapt the rule when the standard percentages don’t fit:

If your needs exceed 50%: Start by scrutinizing what’s in your needs bucket. High rent is often the culprit — and while you can’t always move immediately, you can identify it as the problem and plan around it. Until your housing situation changes, run something like 60/20/20 and protect the 20% savings floor at all costs.

If you have significant high-interest debt: Consider temporarily shifting to 50/20/30 — swapping the wants and savings categories — to accelerate debt payoff. Once high-interest debt is eliminated, restore the 30% wants allocation. Our detailed breakdown of how to use the debt snowball method to wipe out debt faster shows exactly how redirecting just $200–$400 per month from wants to debt payoff can eliminate thousands of dollars of debt within 18 months.

If you’re starting from zero savings: Your first priority within the 20% bucket is a starter emergency fund of $1,000. According to our guide on why 37% of Americans still can’t cover a $400 emergency in 2026, the absence of even a small cash buffer is what forces people into high-interest debt every time something unexpected happens. Get $1,000 saved first — then split the remaining 20% between additional emergency savings and other goals.

The non-negotiable rule within the rule: The 20% savings/debt bucket is protected in every scenario. According to Solutions Bank’s 2026 budgeting analysis, the 20% savings floor is the most important number in the entire framework — protect that before cutting wants. Dropping to 10% or 5% savings to fund a larger wants budget is how budgets fail.

Real Examples: 50/30/20 on Different Incomes

Example 1 — $3,000/month take-home

| Category | Amount |

|---|---|

| Needs (50%) | $1,500 |

| Wants (30%) | $900 |

| Savings/Debt (20%) | $600 |

Needs breakdown: $900 rent, $150 utilities, $250 groceries, $200 car and insurance = $1,500 ✅

Example 2 — $5,000/month take-home

| Category | Amount |

|---|---|

| Needs (50%) | $2,500 |

| Wants (30%) | $1,500 |

| Savings/Debt (20%) | $1,000 |

Savings breakdown: $500 to emergency fund, $300 to Roth IRA, $200 extra toward credit card debt = $1,000 ✅

Example 3 — $7,500/month take-home

| Category | Amount |

|---|---|

| Needs (50%) | $3,750 |

| Wants (30%) | $2,250 |

| Savings/Debt (20%) | $1,500 |

Savings breakdown: $500 emergency fund top-up, $583 Roth IRA (max contribution divided by 12), $417 taxable investment account = $1,500 ✅

The Best Free Tools to Track Your 50/30/20 Budget

You don’t need a spreadsheet or a paid app to run a 50/30/20 budget. These free tools make tracking automatic:

Mint (now Credit Karma) — Links to your bank and credit card accounts, auto-categorizes transactions, and shows you exactly how your spending breaks down each month. Free.

YNAB (You Need a Budget) — The gold standard for people serious about budgeting. It has a 34-day free trial, then costs $14.99/month — worth it once you’ve committed to budgeting seriously.

Your bank’s own app — Most major US banks now include built-in spending categorization and monthly summaries. Check your bank app before downloading anything else.

A simple spreadsheet — Three columns, three rows, one formula per cell. Sometimes the lowest-friction tool is the one you actually use.

The specific tool matters far less than consistent use. Checking your budget takes five minutes. Most people who build a budget and check it weekly stay on track. Most people who set it up once and never look at it don’t.

Why Most First Budgets Fail (And How to Avoid It)

The Centier Bank 2026 budgeting guide points out that the 50/30/20 rule is forgiving by design — it’s not about tracking every single purchase, it’s about building balance between living today and building for tomorrow. The failure mode isn’t picking the wrong percentages. It’s two specific behaviors:

Failure Mode 1 — Quitting after one bad month. Everyone goes over budget sometimes — a car repair, a medical bill, an invitation you said yes to without thinking. One bad month doesn’t mean budgeting failed. It means you had one bad month. Reset and continue.

Failure Mode 2 — Budgeting without automating savings. If your 20% savings contribution requires a manual transfer every month, it will eventually not happen. Set up automatic transfers on payday, before you see the money in your checking account. What you never see, you never miss — and your savings grow without willpower.

The budget works. The system works. The only question is whether you stay in it long enough for it to change your financial life.

FAQ

Q1: What is the 50/30/20 rule for budgeting? A1: The 50/30/20 rule divides your monthly after-tax income into three categories: 50% for needs (housing, utilities, groceries, transportation, insurance, minimum debt payments), 30% for wants (dining out, entertainment, subscriptions, travel), and 20% for savings and extra debt repayment. It’s the most beginner-friendly budgeting framework because it requires no detailed tracking — just three buckets and a monthly check-in.

Q2: How do I start a budget with no experience? A2: Start with three steps. First, calculate your monthly after-tax take-home pay. Second, multiply by 0.50, 0.30, and 0.20 to get your three targets. Third, pull your last month of bank statements and categorize every transaction as a need, want, or savings contribution. Compare your actual spending to your targets and adjust one category at a time.

Q3: Does the 50/30/20 rule work on a low income? A3: It works as a framework, but the percentages need adjustment for low-income households where needs exceed 50% of take-home. The most important number to protect is the 20% savings floor — even on a tight budget, automating any savings contribution, even $25 per week, builds the financial foundation that prevents debt spirals. Adjust the needs and wants percentages before cutting savings.

Q4: What’s the difference between needs and wants in a budget? A4: A need is any expense you cannot reasonably skip without losing housing, health, transportation to work, or the ability to meet minimum debt obligations. A want is anything that improves your life but isn’t required for those basics — dining out, extra streaming services, clothing beyond what you need, hobbies, and travel. The test: could you survive this month without this expense? If yes, it’s likely a want.

Q5: How much should I save each month according to the 50/30/20 rule? A5: The 50/30/20 rule targets 20% of your after-tax monthly income for savings and extra debt payments. On a $4,000 take-home, that’s $800 per month. Priority order within that 20%: first build a $1,000 starter emergency fund, second capture your full employer 401(k) match, third pay down high-interest debt above minimums, fourth continue building emergency savings to 3–6 months of expenses.

DISCLAIMER

This article is for informational and educational purposes only. Individual financial situations vary significantly. The 50/30/20 percentages are guidelines, not rules, and should be adapted to your specific income, expenses, and financial goals. Consider consulting a certified financial planner for personalized budgeting advice.

Mohammad Javed is the founder and personal finance writer behind FinanceBeliever.com. He holds a Master of Commerce (MCom) degree with a specialization in finance and financial markets. Through years of personal experience studying credit systems, debt management, investment strategies, and how everyday financial decisions impact real households, he built Finance Believer to deliver straight, research-backed financial guidance to American readers. Every article he writes is sourced from authoritative data — including the Federal Reserve, the Consumer Financial Protection Bureau, and the Bureau of Labor Statistics. His work covers credit scores, loans, banking, insurance, investing, and personal budgeting — all written in plain English without the jargon.