Let’s do some quick math that might make you a little angry.

If your bank charges a $13 monthly maintenance fee — which is about average right now — you’re paying $156 a year just to have a checking account. Add one or two overdraft fees and you’re easily over $200. Add a few out-of-network ATM charges and you’re pushing $250 to $300 a year.

For what? For the privilege of keeping your own money at their institution.

According to CNBC Select’s June 2026 banking analysis, monthly maintenance fees averaged a record $13.95 in January 2026 — the highest they’ve ever been. According to Amppfy’s March 2026 banking guide, Americans who pay monthly maintenance fees lose around $188 per year on average — before ATM surcharges or overdraft penalties even enter the picture.

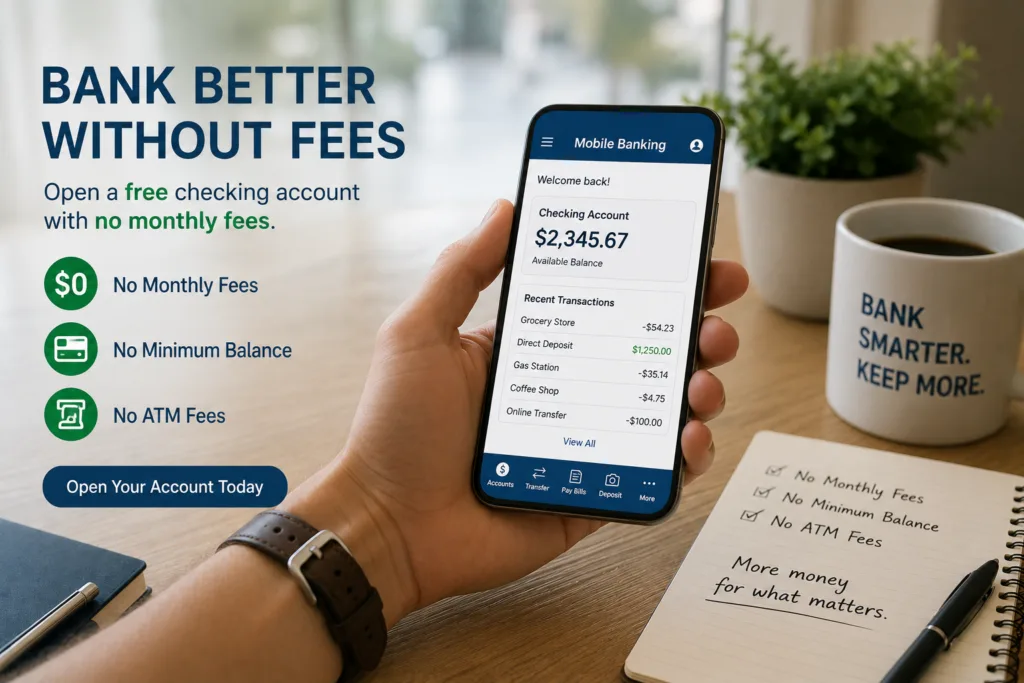

Here’s the part that should actually bother you: the best free checking accounts in 2026 are not the bare-minimum options you settle for when you can’t afford better. They’re genuinely competitive accounts — with early direct deposit, large ATM networks, overdraft protection, and sometimes actual interest on your balance — that happen to charge you nothing.

This guide ranks the 8 best, explains who each one is right for, and tells you exactly what to watch for in the fine print.

What “Truly Free” Actually Means

Before the rankings, let’s be clear about what free actually means — because banks are creative with language.

A truly free checking account has:

- No monthly maintenance fee — ever, under any conditions

- No minimum balance requirement to avoid a fee

- No direct deposit requirement to avoid a fee

- No transaction minimums you have to hit each month

Some accounts advertise as “free” but charge you $12 if your balance drops below $1,500, or $10 if you don’t set up direct deposit. Those aren’t free checking accounts — they’re conditional checking accounts. Every account on this list is free without conditions.

According to Chime’s April 2026 banking analysis, some banks advertise free checking but charge fees if you don’t meet certain conditions — truly free accounts don’t have hoops to jump through.

The 8 Best Free Checking Accounts in 2026

#1 — Chime Checking Account

Best Overall | NerdWallet’s 2026 Winner

Chime has been the dominant no-fee checking account for years, and in 2026 it still deserves the top spot — NerdWallet named it the best checking account overall for 2026.

What makes Chime stand out:

- No monthly fees, no minimum balance, no overdraft fees up to $200 (SpotMe feature)

- Get your paycheck up to two days early with direct deposit

- Access to over 50,000 fee-free ATMs through the Allpoint and Visa Plus Alliance networks

- Automatic savings features that round up purchases and save the difference

The catch: Chime is online-only. There are no branches. If you regularly need to deposit cash, you’ll need to use a retail partner location like Walgreens or CVS, which works fine for most people but is worth knowing upfront.

Best for: Anyone who does most banking on their phone and wants the most features at zero cost.

#2 — Capital One 360 Checking

Best for Hybrid Banking (Online + In-Person)

Capital One is the rare bank that offers genuinely no-fee checking with an actual branch network — over 270 Capital One Café locations and branches across the US, plus one of the best mobile banking apps available.

According to Yahoo Finance’s June 2026 free checking analysis, the Capital One 360 Checking Account has no monthly fees, no minimums, and no overdraft fees, and comes with fee-free overdraft protection options, early direct deposit, and access to more than 70,000 fee-free ATMs.

The mobile app is consistently rated among the highest in the industry — mobile check deposit, instant transaction alerts, card locking, and Zelle built in.

Best for: Anyone who wants the flexibility of in-person banking when needed but primarily banks digitally.

#3 — Ally Bank Spending Account

Best for Interest Earnings

Ally does something most checking accounts don’t: it pays you interest on your balance. Not a lot — but earning something beats earning nothing, and the Ally Spending Account has zero monthly fees, zero minimum balance, and zero overdraft fees.

According to Yahoo Finance’s June 2026 analysis, the Ally Spending Account ranks as one of the best free checking accounts thanks to its zero minimum deposit requirements, no monthly fees or overdraft fees, and ability to earn interest. Ally also reimburses up to $10 per month in out-of-network ATM fees, which covers most casual ATM use.

The limitation: Ally is online-only with no branches and no cash deposit capability. If you regularly handle cash, Ally works better as a secondary account paired with a local bank or credit union.

Best for: People who want to earn a little interest on their checking balance without touching a fee-charging account.

#4 — Discover Cashback Debit

Best for Cash Back on Debit Purchases

Most debit cards earn you nothing. The Discover Cashback Debit account earns you 1% cash back on up to $3,000 in debit card purchases per month — a meaningful perk on a checking account that charges nothing.

According to US News Money’s June 2026 free checking guide, the Discover Cashback Debit account charges no fees to open or maintain, offers fee-free overdraft protection, and provides access to over 60,000 fee-free ATMs. At 1% cash back on $3,000 per month, that’s up to $360 per year in cash back — from a checking account.

Best for: Anyone who uses their debit card frequently for everyday purchases and wants to earn rewards without paying credit card interest.

#5 — SoFi Checking and Savings (Combo Account)

Best for High Interest + Early Paycheck

SoFi pairs checking and savings in one account — which sounds gimmicky until you see the numbers. SoFi members who set up direct deposit can earn up to 3.80% APY on their savings portion while the checking portion remains completely fee-free.

SoFi also pays your direct deposit up to two days early and has a 55,000+ ATM network through Allpoint. No monthly fees, no minimum balance, no overdraft fees for members with direct deposit.

Best for: Anyone who wants to earn high-yield savings rates while keeping everything in one place.

#6 — Axos Rewards Checking

Best for ATM Fee Reimbursements

Axos Bank offers unlimited domestic ATM fee reimbursements on their Rewards Checking account — which matters a lot if you travel frequently or live somewhere without easy access to a fee-free ATM network.

The account is truly free with no monthly maintenance fee, and you can earn up to 3.30% APY on balances with the right combination of account activities. The activity requirements for maximum APY are more involved than the other accounts on this list, so check the current requirements before opening.

Best for: Frequent travelers or anyone who regularly uses ATMs outside the major fee-free networks.

#7 — American Express Rewards Checking

Best for Debit Rewards + Points

American Express entered the checking account space with a competitive product that earns Membership Rewards points on debit purchases — something almost no other checking account offers.

According to Yahoo Finance’s June 2026 analysis, the American Express Rewards Checking account earns 1% APY and 1 Membership Rewards point for each $2 of eligible debit card purchases, with no monthly fees and access to 70,000+ fee-free ATMs. If you already collect Amex points through a credit card, pooling them from a checking account adds up meaningfully over time.

The limitation: no cash deposits, and the account requires an existing American Express relationship to open.

Best for: Existing Amex cardholders who want to earn points on everyday debit spending.

#8 — Connexus Simply Free Checking (Credit Union)

Best for a Basic No-Frills Free Account

Sometimes you just want a checking account that does what a checking account is supposed to do — holds your money, lets you spend it, charges you nothing, and gets out of your way.

The Connexus Simply Free Checking does exactly that. No monthly fees, no minimum balance, free overdraft transfers, and access to the same surcharge-free ATM network as the premium Connexus account. It doesn’t earn interest, but it doesn’t cost you anything either.

Best for: Anyone who wants the simplest possible free checking account without features they won’t use.

Side-by-Side Comparison

| Account | Monthly Fee | Min. Balance | ATM Network | Early Deposit | Interest/Rewards |

|---|---|---|---|---|---|

| Chime | $0 | $0 | 50,000+ | ✅ Up to 2 days | ❌ |

| Capital One 360 | $0 | $0 | 70,000+ | ✅ Up to 2 days | Small interest |

| Ally Spending | $0 | $0 | 43,000+ (reimburses $10/mo) | ✅ Up to 2 days | ✅ Interest |

| Discover Cashback Debit | $0 | $0 | 60,000+ | ❌ | ✅ 1% cash back |

| SoFi Checking | $0 | $0 | 55,000+ | ✅ Up to 2 days | ✅ Up to 3.80% APY |

| Axos Rewards | $0 | $0 | Unlimited reimburse | ✅ Up to 2 days | ✅ Up to 3.30% APY |

| Amex Rewards Checking | $0 | $0 | 70,000+ | ❌ | ✅ 1% APY + points |

| Connexus Simply Free | $0 | $0 | Shared CU network | ❌ | ❌ |

Hidden Fees to Watch For Even in “Free” Accounts

Free monthly maintenance doesn’t mean zero fees ever. Watch for these even in no-fee accounts:

Overdraft fees — Some accounts charge $25 to $35 per overdraft even with no monthly fee. Chime and SoFi offer overdraft protection to eligible members. Ally has no overdraft fees at all.

Out-of-network ATM fees — Most free checking accounts waive fees at their own network. Outside that network, your bank may not charge you, but the ATM operator still might charge $3 to $5. Check whether the account reimburses these.

Paper statement fees — Some accounts charge $1 to $3 per month if you want a mailed statement. Go paperless and this disappears.

Wire transfer fees — Most checking accounts charge $15 to $30 for outgoing domestic wire transfers. If you wire money regularly, check this before opening.

Inactivity fees — A handful of accounts charge fees if you don’t use them for several months. Check the fee schedule before leaving an account dormant.

The Right Way to Switch Banks

Switching checking accounts feels complicated — but it’s straightforward if you do it in the right order.

Open the new account first. Get it set up, verify your identity, and confirm the routing and account numbers. Then redirect your direct deposit to the new account through your employer’s payroll portal. Then update any automatic bill payments to pull from the new account. Finally, once all outstanding checks have cleared and automatic transactions have moved over, close the old account.

According to Amppfy’s March 2026 switching guide, don’t leave small amounts behind when closing — banks have been known to charge inactivity fees on dormant accounts with minimal balances, eventually sending the remaining funds to state unclaimed property programs. Transfer every dollar to zero before closing.

The whole process takes two to four weeks if you’re methodical about it. The $188 per year you stop losing makes it worth every minute.

Free Checking as Part of a Bigger Financial Picture

Eliminating a $13 monthly checking fee doesn’t change your financial life on its own. But it’s part of the same mindset shift that does change it — finding and eliminating every dollar you’re spending on nothing, then redirecting those dollars toward something that actually moves your situation forward.

If you’re working on building better money habits overall, our complete guide to how to budget money using the 50/30/20 rule shows you how to structure your income so your checking account becomes a tool rather than a drain. And if you want to make your savings actually work while you sleep, our breakdown of the best high-yield savings accounts versus money market accounts in 2026 shows you where to keep the money you’re not spending — so it grows at 4% to 5% instead of sitting at 0.01%.

The checking account is where your money lives between paychecks. It should cost you exactly nothing.

FAQ

Q1: What is the best free checking account in 2026? A1: NerdWallet named Chime the best checking account overall for 2026, citing its zero fees, SpotMe overdraft protection up to $200, early direct deposit, and 50,000+ fee-free ATMs. Capital One 360 Checking is the top pick for anyone who wants both online and in-person banking options with no fees. The best account depends on whether you prefer online-only banking or need access to physical branches.

Q2: Are free checking accounts actually free? A2: Truly free checking accounts have no monthly maintenance fee under any conditions — no minimum balance, no direct deposit requirement, no transaction minimum. Some accounts advertise “free” checking but charge fees if you don’t meet certain conditions. The accounts on this list are free without conditions, though all accounts may have fees for specific services like wire transfers or paper statements.

Q3: What is the average monthly fee for a checking account in 2026? A3: According to CNBC Select, monthly maintenance fees averaged a record $13.95 in January 2026 — the highest ever recorded. Amppfy’s analysis found the average American who pays these fees loses approximately $188 per year before ATM surcharges or overdraft penalties are included. Switching to a no-fee checking account eliminates this cost entirely.

Q4: Do free checking accounts have good ATM access? A4: Yes — the best no-fee checking accounts in 2026 have extensive ATM networks. Capital One 360 and American Express Rewards Checking provide access to over 70,000 fee-free ATMs. Chime has 50,000+ through Allpoint and Visa Plus Alliance. Axos Rewards reimburses all domestic ATM fees with no limit. Most Americans will find a fee-free ATM within easy reach regardless of which account they choose.

Q5: Can I switch checking accounts without losing money or missing payments? A5: Yes, with the right approach. Open the new account first, then redirect direct deposit through your employer’s payroll portal, then update automatic bill payments to the new account, then let outstanding checks clear from the old account before closing it. The process typically takes two to four weeks and is completely safe as long as you don’t close the old account before all transactions have migrated to the new one.

DISCLAIMER

Account features, fees, ATM networks, and interest rates change frequently. The information in this article is based on data available as of June 2026. Always verify current terms directly with each bank before opening an account. Finance Believer is not a bank and does not endorse any specific financial institution.

Mohammad Javed is the founder and personal finance writer behind FinanceBeliever.com. He holds a Master of Commerce (MCom) degree with a specialization in finance and financial markets. Through years of personal experience studying credit systems, debt management, investment strategies, and how everyday financial decisions impact real households, he built Finance Believer to deliver straight, research-backed financial guidance to American readers. Every article he writes is sourced from authoritative data — including the Federal Reserve, the Consumer Financial Protection Bureau, and the Bureau of Labor Statistics. His work covers credit scores, loans, banking, insurance, investing, and personal budgeting — all written in plain English without the jargon.